California has never been an easy market for fix-and-flip investors. Land is scarce, labor is expensive, permit offices are slow, and the buyers your finished product needs to impress have seen a lot of renovations. What California does offer — and this matters — is resale prices that can absorb a meaningful rehab budget and still leave a real return on the other side.

In 2026, that calculus is shifting in ways that require precision. Gross flip margins nationally have compressed to their tightest levels since 2008, according to ATTOM data. California markets are not immune. But investors who understand the actual cost structure — not national averages, not what a podcast said two years ago — are still closing profitable deals. The ones getting hurt are the ones working with outdated numbers.

This article gives you the real figures, market by market, with enough context to run your own deal math.

The statewide picture first

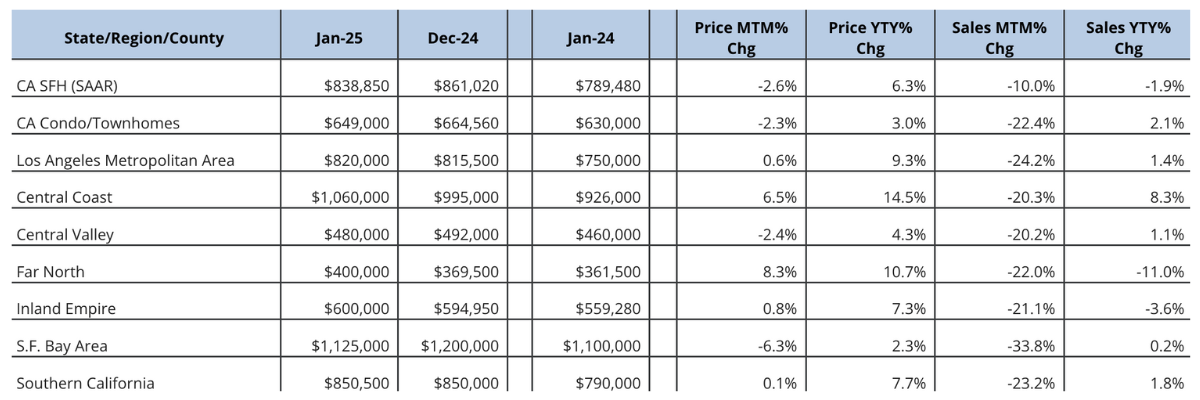

California’s residential market in 2026 is running hotter than many anticipated. According to the California Association of Realtors, the statewide median sale price for existing single-family detached homes hit $930,260 in May 2026 — up from $822,630 in January and tracking well ahead of where most analysts expected the year to land. That is a meaningful acceleration from the subdued price environment of late 2025, when the statewide median was ranging between $850,000 and $890,000.

For investors, there are a few structural facts from the current CAR data worth holding onto:

Inventory is tightening again. The statewide Unsold Inventory Index — which measures how many months it would take to sell all available listings at the current pace — stood at 3.4 months in May 2026, down from a peak of 4.4 months in January. That compression signals strengthening buyer demand heading into summer, and it is showing up in prices. A reading below 4 months generally indicates a seller-favoring market.

Sales volume is stabilizing. After a choppy start to the year — statewide YoY sales were negative in January — volume recovered in spring 2026. Most key investor markets logged positive or flat YoY sales comparisons by April and May, suggesting the market is absorbing inventory at a reasonable pace. That is a positive sign for investors planning six-month holds.

Foreclosure activity is rising, but from a very low base. Q1 2026 foreclosure filings remain at roughly one-eighth of their 2009–2011 peak. California’s non-judicial foreclosure process — averaging about eight months from notice of default to REO — means Q1 NODs will begin producing distressed inventory in late 2026. That is a pipeline worth watching for off-market acquisition opportunities.

Market-by-market: the four regions that matter most

California is not one market. A deal structure that works in Riverside looks nothing like one in West Adams. Here is where we actually lend and what the numbers look like on the ground.

What rehab actually costs in California

This is where California investors most often get into trouble — not on the acquisition side, but on the rehab side, where national benchmarks and YouTube renovation budgets collide with California reality.

California renovation costs currently run approximately 35–45% above the national average. The reasons are structural and unlikely to change: licensed trade labor commands a significant premium (electricians and plumbers billing $130–$185 per hour in the coastal metros), Title 24 energy code compliance adds cost to every project that touches HVAC, lighting, or the building envelope, and permitting timelines in many counties routinely extend project duration by 8–16 weeks.

| Scope of Work | National Avg. / SF | CA Coastal Range | CA Inland Range |

|---|---|---|---|

| Cosmetic only (paint, flooring, fixtures, landscaping) | $15 – $30 | $28 – $55 | $20 – $40 |

| Moderate (cosmetic + kitchen, baths, HVAC service) | $40 – $80 | $75 – $150 | $55 – $110 |

| Full gut renovation (systems, layout changes, all finishes) | $80 – $150 | $150 – $300+ | $110 – $200 |

| Kitchen remodel (mid-grade) | $35,000 avg. | $55,000 – $90,000 | $40,000 – $65,000 |

| Primary bath remodel | $12,000 – $25,000 | $22,000 – $50,000 | $16,000 – $35,000 |

| Electrical panel + rewire (older home) | $8,000 – $18,000 | $15,000 – $35,000 | $12,000 – $25,000 |

| Roof replacement (composition, 1,500 SF) | $8,000 – $14,000 | $14,000 – $28,000 | $11,000 – $20,000 |

The benchmarks above reflect what investors pay when they hand a project to a general contractor and step back. The most cost-effective operators in California don’t work that way. Here is what we consistently see from experienced borrowers who keep their numbers lean:

Investors who are licensed in a trade — or who have the experience and legal standing to self-perform work — eliminate the GC markup entirely on the scopes they handle themselves. On a moderate renovation, GC overhead and profit typically runs 15–25% on top of subcontractor costs. Removing that layer materially changes the math.

Cutting out the general contractor and hiring subcontractors directly — electricians, plumbers, framers, tile setters — is the most common cost-control move among high-volume California flippers. It requires more management time and coordination, but experienced investors who have built reliable sub relationships often run projects 20–30% under GC-managed budgets on comparable scopes.

Retail markup on materials — flooring, cabinetry, fixtures, appliances — is a significant and frequently overlooked cost on flip projects. Investors who open trade accounts at flooring distributors, kitchen wholesalers, and plumbing supply houses often pay 30–50% less than retail on the same product. On a full kitchen and bath renovation, that gap can be $15,000–$30,000.

Most institutional construction lenders require a licensed general contractor on every project — a condition that adds cost and removes flexibility from experienced investors who don’t need one. At Lantzman Lending, we do not require borrowers to use a general contractor on fix-and-flip loans. If you have the experience, the subcontractor relationships, and the project management capability to run the job yourself, we’ll work with your structure. That flexibility is a direct advantage for investors who have spent years building the skills and relationships that allow them to control costs at a level a first-time buyer cannot.

Running the deal math by market

Abstract percentages don’t finance deals — actual dollar amounts do. Below are realistic deal models for each of our four key markets, using conservative inputs that reflect what we see on the ground in 2026. These are illustrative scenarios, not guarantees, but they reflect the actual deal flow we review.

San Diego — Coastal neighborhood, 3/2, 1,400 SF

San Diego’s strong price appreciation in 2026 (+5.8% YoY) and tight supply make it a compelling flip market — but entry is demanding. Finding a distressed 3/2 in a coastal neighborhood for under $730,000 requires either off-market sourcing or deep knowledge of estate sales, probate situations, and pre-foreclosure leads. Deals exist; they are not on the MLS at that price. Investors working in San Diego need a lender who can move as fast as the market does — same-day review and 48-hour closes are the baseline, not a premium.

Los Angeles — Mid-city or East LA, 3/2, 1,200 SF

Los Angeles is a city of submarkets. A deal model that makes sense in Glassell Park looks completely different from one in Bel Air or Boyle Heights. The January 2025 wildfires continue to affect insurance availability and pricing in affected communities, which can meaningfully alter holding costs and buyer pool in fire-adjacent zones. Work with a local insurance broker before underwriting any deal in the western San Fernando Valley or west LA hillsides.

Sacramento — Suburbs, 3/2, 1,500 SF

Sacramento is the market most worth watching in 2026. The April CAR data shows Sacramento County posting +8.3% year-over-year sales volume growth — the strongest of our four markets — while the UII of 2.6 months in April signals genuine inventory tightness. Rehab costs are meaningfully lower than coastal California (skilled trades are more available, permitting timelines shorter), and the buyer pool is expanding. The one caution: San Bernardino County (UII 5.1) and parts of Sacramento’s outer suburbs are seeing more supply, which means finished product needs to be priced correctly and presented well. The days of selling a mediocre renovation at full ask are over in the Sacramento suburbs.

Inland Empire — Riverside, 4/2, 1,600 SF

The Inland Empire remains the highest-volume flip market in Southern California and the most accessible for investors who are building their first or second project portfolio. Affordability migration from coastal counties continues to sustain buyer demand. The new construction pipeline is the main risk factor — Riverside and San Bernardino counties are two of the highest-construction-activity markets in the state, which eventually creates competition for your resale. Focus on existing neighborhoods with good schools and walkable amenities; new builds can’t compete there on character or lot size.

The formula every California flipper needs to know cold

You have probably heard of the 70% rule: never pay more than 70% of ARV minus rehab costs. In most of the country, that is a reasonable starting point. In California, it is the wrong number — and using it rigidly will cause you to walk away from deals that actually work, or worse, to misread why you lost a competitive offer.

California’s high ARV prices fundamentally change the math. On a $1,100,000 resale, the fixed costs of transacting — title, escrow, agent commissions, transfer tax, staging — are simply larger in absolute dollars than on a $300,000 flip in Ohio. But they do not scale proportionally to ARV. That asymmetry is what allows California investors to work at higher percentage thresholds and still achieve acceptable margins.

In practice, experienced California operators use a range of 70% to 82% of ARV minus construction costs, depending on the price point, market velocity, rehab scope, and exit certainty. Many investors targeting a 10–12% net profit margin will underwrite to 80–82% less construction on well-located coastal assets, knowing that the absolute dollar spread at that ARV still produces a meaningful return.

Example at 80%: ARV $1,100,000 · Construction $154,000 · Acquisition = ($1.1M × 0.80) − $154K = $726,000 max

Full costs (2pt origination, buy closing, 9% interest on loan, holding, sell closing) consume ~$120,000–$130,000 → leaves ~8–9% net profit.

Example at 72%: ARV $580,000 · Construction $100,000 · Acquisition = ($580K × 0.72) − $100K = $318,000 max

Lower price tiers carry proportionally heavier fixed costs — the tighter entry percentage protects the margin.

How the percentage adjusts by price tier

This is the nuance most out-of-state content misses entirely. California’s transaction costs are largely fixed in dollar terms (escrow, title, county transfer tax) or scaled to a flat commission rate (agent fees). At a $500,000 ARV, those costs consume a larger share of the spread than at a $1,200,000 ARV. That is why the formula shifts as you move up the price ladder.

| ARV Range | Typical % Used | Target Net Margin | Why This Tier Works This Way |

|---|---|---|---|

| Under $500K (Inland Empire / Sacramento entry) | 68% – 72% | 10% – 14% | Transaction costs are proportionally heavier; thinner absolute spread requires tighter entry |

| $500K – $750K (Inland Empire / Sacramento mid) | 72% – 76% | 10% – 13% | More room to work; rehab costs still manageable relative to exit price |

| $750K – $1M (LA suburbs / SD inland / Sacramento luxury) | 75% – 79% | 10% – 12% | Higher absolute dollar spread absorbs fixed costs; competition for product is strong |

| $1M – $1.5M (coastal LA / San Diego proper) | 78% – 82% | 10% – 12% | Large absolute spread justifies higher entry; well-executed product moves quickly in this tier |

| $1.5M+ (luxury coastal) | Case by case | Varies widely | Days on market and buyer pool depth become the dominant risk variables; underwrite conservatively |

One critical note on ARV methodology that applies at every price tier: always use closed comparable sales within the last 90 days and within a tight geographic radius — preferably the same neighborhood and same configuration. Active listings are not comps. California appraisers and experienced buyers’ agents know their markets in granular detail. An ARV inflated by outdated sales, a different submarket, or a different product type is one of the fastest ways to turn a deal that looked like 11% margin into a breakeven or a loss.

What the timeline actually looks like

California investors frequently underestimate project duration, and every additional month costs real money in interest. A realistic timeline for a moderate renovation in California looks like this:

Weeks 1–2: Due diligence, contractor walk-throughs, finalizing scope of work. If you haven’t built your contractor relationships before going under contract, you’re already behind.

Weeks 2–6: Permit submission and plan check. Simple cosmetic-only projects often don’t require permits. Any structural, electrical, or plumbing work does. Count on 4–10 weeks in most California jurisdictions for standard permits; coastal cities and some Bay Area municipalities run longer.

Weeks 6–20: Active construction. A well-managed moderate renovation on a 1,200–1,600 SF home runs 10–14 weeks with a reliable crew. Add 2–4 weeks as buffer for material lead times, inspection scheduling, and the subcontractor gaps that will happen on every job.

Weeks 20–26: Listing, escrow, close. California residential closings typically run 21–30 days once in escrow. Budget 2–4 weeks from listing to accepted offer in a normal market.

A 6-month hold is a reasonable planning assumption for a straightforward moderate renovation. Full gut projects easily run 9–12 months. Model your financing costs accordingly.

Where California flippers find the deals

On-market distressed listings in California are increasingly rare and increasingly competitive. The MLS is not where experienced investors find their best deals in 2026. The most reliable sources:

Probate and estate sales. California’s aging population creates a steady flow of estate-owned properties that often require updating and are sold by executors and professional fiduciaries who prioritize certainty of close over maximum price. This is one of the most consistent sources of below-market inventory in the state — particularly in established neighborhoods in San Diego, the San Fernando Valley, and the Sacramento suburbs.

Pre-foreclosure outreach. With NOD filings rising from their pandemic lows, homeowners in default represent an opportunity for investors who can offer a fast, certain close. This requires direct mail or driving neighborhoods to identify properties, and the ability to move quickly once contact is made.

Direct mail and driving for dollars. Deferred maintenance is visible from the street. Investors who systematically work their target neighborhoods — sending letters to owners of visibly distressed properties — generate a small but consistent stream of off-market leads.

Wholesale networks. California has an active community of wholesalers who source and assign distressed contracts. The assignment fees have risen in recent years, which compresses margins, but the deal flow can be valuable for investors who are still building their direct lead generation pipeline.

The financing structure that fits California flips

Conventional financing does not work for fix-and-flip projects. Banks do not lend on properties in poor condition, and the timelines required to close a distressed acquisition — often 7–21 days when competing with cash buyers — cannot be met by any institutional lender.

Private bridge loans are the correct tool for this strategy, and the structure matters. Here is what California investors should be evaluating when they choose a lender:

Speed of approval and close. A deal with a 10-day escrow needs a lender who can issue a same-day term sheet and close within 48–72 hours of a clean title report. This rules out most institutional capital.

Loan-to-value and loan-to-cost. Most private lenders in California will lend up to 65–75% of ARV, covering both purchase and a portion of the rehab. The rehab draw structure is critical: a lender who holds back 100% of renovation funds until completion creates a cash-flow problem for investors who need to pay contractors in phases.

Draw management. In-house draw management — where your lender can inspect and release renovation draws quickly — directly affects your project timeline. Slow draws mean you’re paying contractors late, which means your project slows down or your crew moves on to another job.

No prepayment penalties. If you sell faster than projected — a good problem to have — you should not be penalized for it. Many lenders build prepayment penalties into their note; negotiate these out, or choose a lender who doesn’t use them.

Interest-only payments. Standard on private bridge loans. You should not be paying down principal on a 6-month renovation loan.